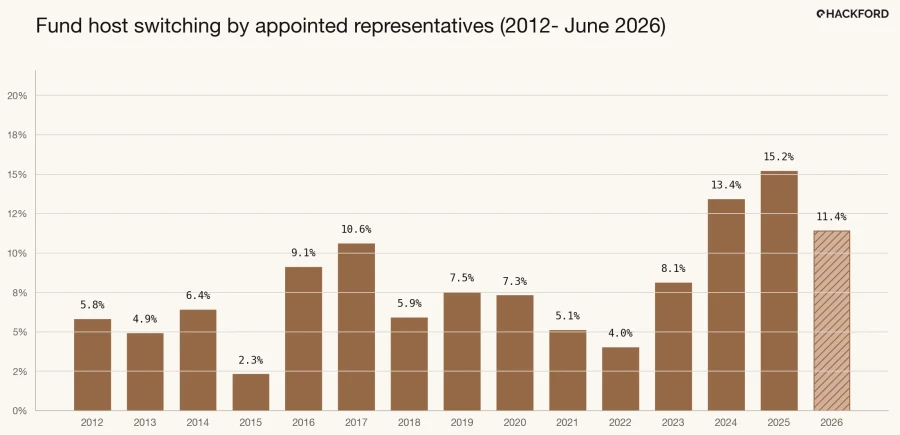

Fund adviser ARs are switching regulatory hosts at record rates.

Switching has been on the rise since 2022. Last year saw a record 15.2% of ended AR-principal relationships followed by the AR appearing under another confirmed fund host. This year could surpass it if the current trajectory holds: 11.4% have already switched, with H1 still incomplete.

Source: Hackford analysis of FCA Register Extract Service data.

Why switching may be rising

A working theory is that switching is rising because the market is becoming more operationally intensive, pushing it towards scale at one end and specialisation at the other.

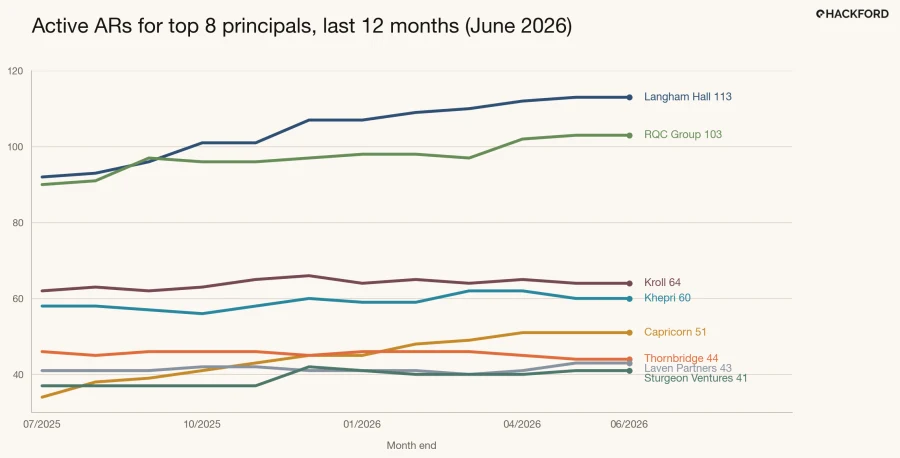

The chart of active ARs among the eight largest hosts shows that only the two very largest are growing. Capricorn looks like an exception only if viewed separately from RQC.1

Both Langham Hall and RQC/Capricorn have been growing, supporting the theory that the largest firms have the scale and infrastructure to attract and retain business in a more operationally demanding environment. More oversight and more regulatory scrutiny favour hosts with the right infrastructure.

Why switching could increase

If HMT reforms to the AR regime increase oversight demands, some hosts may decide the economics no longer work as fixed costs rise. A reduction in the number of hosts is unlikely to show up immediately; 2028 will be the year to watch.

Also, many of the existing ad hoc arrangements could be dropped. Being a fund manager with a few appointed representatives on the side will seem less attractive when it requires more focused oversight.

Splitting in three

If AR regime changes come into effect, there are three positions to watch.

The incumbents have scale. They can absorb higher oversight demands, use existing infrastructure, and spread fixed costs across a larger AR base.

The challengers can continue to win new ARs if they are meaningfully differentiated from the larger platforms. That might come from sector focus, service model, technology, or speed of execution.

That leaves the middle: too small to win on scale, but not differentiated enough to avoid competing with scale.

It is a dangerous time to be in the middle.

1. Capricorn is best read alongside RQC. Capricorn announced it had acquired a majority stake in Robert Quinn Consulting in late 2019. It was rebranded to RQC Group in 2020. Taken together, the two firms accounted for over 150 ARs in June 2026. ↩